- Contact Us Now: 754-400-5150 Tap Here to Call Us

Robo-Verifier Lona Hunt Admits, Twice, to Not Even Reading Complaint Before Signing Under Penalty of Perjury

The entire reasoning behind the Florida Supreme court taking unprecedented, historic action to amend rule 1.100(b) back in 2010 was because of the financial industry’s well documented illegal behavior. It was enacted around the time that the “robo signing” scandal had broken wide open. We now know that “robo-signing” is used to describe the process of having a person sign a document without authority to do so and/or knowledge as to that which she/he is signing, despite swearing otherwise. The “robo-signing” scandal set off a nation-wide foreclosure moratorium and ultimately led to settlements with 49 states, Office of the Comptroller of the Currency consent orders, and numerous class action and shareholder lawsuits. Mortgage foreclosure related settlements with Ocwen, LPS, Chase and others continue to roll in. Yet, no matter the amount and severity of lawsuits, settlements, and bad publicity, it appears, at least in this case, that the act of signing without proper authority or knowledge as to that which one is signing, continues. Ms. Hunt freely admitted, twice, to not reading the foreclosure complaint before signing it. Further, with her limited knowledge, it was impossible for her to truthfully and accurately verify all the facts alleged in the complaint.

Fla. R. Civ. P. 1.110(b) states in relevant part:

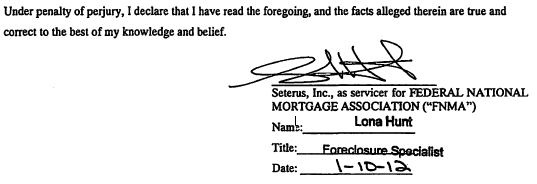

When filing an action for foreclosure of a mortgage on residential real property the complaint shall be verified. When verification of a document is required, the document shall include an oath, affirmation, or the following statement: “Under penalty of perjury, I declare that I have read the foregoing, and the facts alleged therein are true and correct to the best of my knowledge and belief.”

The complaint in this case contained the above quoted language and was signed by Lona Hunt, Foreclosure Specialist for Seterus, Inc., the alleged servicer and foreclosure arm for Plaintiff, Federal National Mortgage Association (Fannie Mae).

The deposition of Lona Hunt took place on October 17, 2014, during which time Ms. Hunt was questioned about her knowledge of the truth and accuracy of the facts in the foreclosure complaint, which she allegedly verified. During the deposition, Ms. Hunt admitted twice that she did not read the complaint, even though she swore in the complaint, under penalty of perjury, that she had.

Mr. Rosen: Q. Let’s take a look at the complaint. First of all, before you signed, did you read the complaint?

Lona Hunt: A. No

(Hunt Depo, P. 43 Ln. 10-13).

Later, when questioned by Plaintiff’s counsel, Ms. Hunt again admitted to not reading the complaint.

P’s Counsel: Q. Okay. Now, when you received that complaint, the draft to review for execution, did you read it first?

Lona Hunt: A. No.

(Hunt Depo, P. 55 Ln. 18-21).

It is clear that the witness understood the question posed and answered truthfully; she did not read the complaint before signing the verification. At the beginning of the deposition, Defendants’ counsel advised Ms. Hunt to verbalize when she didn’t understand a question and Ms. Hunt agreed. (Hunt Depo, P. 13 Ln. 19-25). At least twenty-three times during the relatively short deposition, Ms. Hunt stated that she either did not understand certain questions or asked counsel to repeat. (Hunt Depo, P. 8 Ln. 10, P. 9 Ln. 21, P. 11 Ln. 4, P. 19 Ln. 15, P. 20 Ln. 11, P. 20 Ln. 17, P. 22 Ln. 6, P. 22 Ln. 18, P. 25 Ln. 23, P. 26 Ln. 23, P. 31 Ln. 18, P. 38 Ln. 1, P. 42 Ln. 12, P. 42 Ln. 24, P. 44 Ln. 5, P. 44 Ln. 9, P. 45 Ln. 11, P. 48 Ln. 24, P. 52 Ln. 2, P. 53 Ln. 10, P. 53, Ln. 16, P. 57 Ln. 9, P. 59 Ln. 3). However, when asked if she read the complaint, once by Defense counsel and once by Plaintiff’s counsel, Ms. Hunt did not need clarification and did not hesitate to answer. The answer and the truth came right out.

Plaintiff’s counsel then lead Ms. Hunt to agree that she had read it as she was going through to “verify the various facts.”

P’s Counsel: Q. Did you read it as you were going through to verify the various facts that are set forth in the complaint?

. . .

Lona Hunt: A. Yes.

(Hunt Depo. P. 55 Ln. 22 – Pg. 56 Ln. 3)

Ms. Hunt’s agreement that she read it as she was going through to “verify the various facts” related only to the fact that Ms. Hunt scanned the complaint to verify Defendant’s name, the county, the UPB, and the date of default.

Mr. Rosen: Q. What is it that you were looking for to compare between the verified complaint and what was on the computer?

Lona Hunt: A. Defendant’s name, the county.

. . .

Mr. Rosen: Q. The defendant’s name, the county?

Lona Hunt: A. The UPB and the date.

Mr. Rosen: Q. And that’s the date of?

Lona Hunt: A. The default.

Mr. Rosen: Q. Okay. Anything else that you were looking at between the verified complaint and what was on the computer screen?

. . .

Lona Hunt: A. No.

Mr. Rosen: Q. What was on the computer screen?

Lona Hunt: A. Their loan number, their name, their address, their UPB and the default date.

Mr. Rosen: Q. And was that through that PULS system as well?

Lona Hunt: A. Yes

(Hunt Depo, P. 36 Ln. 15 – P. 37 Ln. 16).

Mr. Rosen: Q. Was there anything else you looked at other than the PULS report when also looking at the complaint?

. . .

Lona Hunt: A. The note and mortgage.

Mr. Rosen: Q. Anything else?

Lona Hunt: A. No.

(Hunt Depo, P. 38 Ln. 3-10).

Even if Ms. Hunt had read the complaint before signing it, she admitted that she could not verify the truth and accuracy of the alleged facts in paragraphs 1, 2, 3, 4, 5, 6, 8, 9, and 10 as well as in the “wherefore” clause of the Complaint. Although Ms. Hunt signed the verification on the Complaint under penalty of perjury and swore that all of the facts alleged in the Complaint were true and correct to the best of her knowledge and belief, she admitted numerous times in her deposition that she did not know the facts she was verifying, did not understand the words used in the complaint, and/or could not accurately describe where the information for those facts came from.

The Complaint and Ms. Hunt’s testimony are as follows, respectively.

Paragraph 1 of Complaint states “. . . All conditions precedent to the filing of this matter have been completed and/or waived.” Ms. Hunt admitted that she did not know what this meant:

Mr. Rosen: Q. And also in paragraph 1 there is the word “condition precedent.” What does condition precedent mean?

. . .

Lona Hunt: A. I’m not sure.

. . .

Mr. Rosen: Q. I just want to know if you know what that means?

Lona Hunt: A. I don’t understand, no.

Mr. Rosen: Q. Okay. You understand my question, you just don’t understand what condition precedent means, is that what you’re saying?

Lona Hunt: A. Yes.

Mr. Rosen: Q. How did you know, if at all, whether or not conditions precedent to the filing of this matter had been completed or waived, if you knew?

. . .

Lona Hunt: A. I didn’t know. I don’t know.

(Hunt Depo, P. 43 Ln. 20 – P. 45 Ln. 3).

Paragraph 2 of the Complaint states that “[t]he subject-property is owned by Defendant(s), Redacted, who hold(s) possession.” Ms. Hunt’s testimony regarding paragraph 2 reveals that she is not familiar with very the basic principles of Plaintiff’s business, such as ownership of property, as she could not properly identify the document which indicated that Defendant was the record owner of the subject property.

Mr. Rosen: Q. Okay. In paragraph 2 it says subject property owned by defendant Redacted. How do you know that or do you know that?

Lona Hunt: A. The mortgage and the note.

Mr. Rosen: Q. And something in the mortgage and note tells you that they own – that Redacted owns the subject property?

. . .

Lona Hunt: A. Yes

(Hunt Depo, P. 45 Ln. 4-15).

Paragraph 3 of the Complaint states that unknown tenants in possession may claim an interest in the subject property by virtue of possession or occupancy; however their claims are subordinate, junior and inferior to the Plaintiff’s interests. Ms. Hunt admitted that she did not know if tenants were in possession and further did not know what it meant to be subordinate, junior or inferior to Plaintiff’s lien. After reading paragraph 3, Ms. Hunt was asked:

Mr. Rosen: Q. Did you know if that was the case that there were any tenants in possession of the property?

Lona Hunt: A. No.

Mr. Rosen: Q. And what does it mean to be subordinate, junior and inferior to the lien of plaintiff’s mortgage?

. . .

Lona Hunt: A. I’m not sure.

(Hunt Depo, P. 45 Ln. 25 – P. 46 Ln. 7).

Similarly, Ms. Hunt did not know the truth or accuracy of Paragraph 4 of the Complaint, which states that unknown spouses, heirs, devisees, etc. may have an interest in the subject property which is subordinate, junior and inferior to Plaintiff’s.

Mr. Rosen: Q. And in the next paragraph, paragraph 4, that in addition to all other defendants and it says, “Unknown spouses heirs, devisees, grantees, assignees, creditors, trustees, successors in interest or other parties claiming interest in the subject property by, through or against any said defendants, whether natural or corporate, who are not known to be alive or dead, dissolved or existing, are joined as defendants herein.” How did you know about those other specifically – how did you know that that was the case?

. . .

Lona Hunt: A. I don’t know.

Mr. Rosen: Q. Okay. It then says, “The claims of said parties are subject, subordinate and inferior to the interest of the plaintiff.” How did you know that that was correct?

. . .

Lona Hunt: A. I didn’t know.

(Hunt Depo, P. 46 Ln. 9 – P. 47 Ln. 3).

Paragraph 5 of Plaintiff’s Complaint states that Defendants, Mr. and Mrs. Redacted, “executed and delivered a mortgage securing payment of the note to JPMorgan Chase Bank, N.A.” Ms. Hunt did not know what that meant.

Mr. Rosen: Q. What does it mean securing payment of the note to JPMorgan Chase Bank, N.A., what does that mean?

Lona Hunt: A. That’s who had it. I’m not for sure.

(Hunt Depo, P. 48 Ln. 3-6).

Paragraph 5 further alleged that the mortgage mortgaged the property “then owned and in possession of the mortgagor(s).”

Mr. Rosen: Q. And how did you know that the property described in the mortgage was owned and in possession –or who owned it and who was in possession of it?

Lona Hunt: A. Fannie Mae.

Mr. Rosen: Q. How did you know that?

. . .

Lona Hunt: A. The Note.

Mr. Rosen: Q. So, just to clarify, I’m asking you how did you know who owned and was in possession of the property at the time of – at the time of origination?

Lona Hunt: A. Please repeat.

Mr. Rosen: Q. Sure. I’m asking how did you know who owned the property and who possessed the property at the time of origination?

Lona Hunt: A. By the note. I can’t look at the page.

Mr. Rosen: Q. Let’s take a look at the note. It’s attached to the complaint, Exhibit B. Can you show me where in the note it says who owned and possesses the property?

. .

Lona Hunt: A. Federal National Mortgage Association, the back page.

Mr. Rosen: Q. The back page it’s telling you who owns the property?

Lona Hunt: A. It says pay to the order of Federal National Mortgage Association.

(Hunt Depo, P. 48 Ln. 11 – P. 49 Ln. 15).

Here, Ms. Hunt further demonstrated her lack of competency to verify the Complaint as she was clearly confused with the concept of ownership of the property versus ownership of the note, despite the fact that Defendants’ counsel asked Ms. Hunt multiple times specifically about the property. Further, Ms. Hunt could not have verified paragraph 5 as she admitted that she did not even understand the term “mortgagor.”

Mr. Rosen: Q. Okay. What does it mean to be the mortgagor?

. . .

Lona Hunt: A. I’m not sure.

(Hunt Depo, P. 49 Ln. 16-23).

Paragraph 6 of Plaintiff’s Complaint states that “Plaintiff is the owner and holder of the note.” Although Ms. Hunt correctly identified the endorsement on the note as payable to Fannie Mae, she admitted that she had no idea what that meant.

Mr. Rosen: Q. How did you know that Fannie Mae is the owner and holder of the note?

Lona Hunt: A. The note where it’s stamped at the back saying that Fannie Mae – pay to the order of Fannie Mae in our system.

Mr. Rosen: Q. Okay. What does it mean to be an owner and holder of a note?

. . .

Lona Hunt: A. I’m not – I’m not quite sure. Don’t know.

(Hunt Depo, P. 49 Ln. 25 – P. 50 Ln. 9).

Paragraph 8 of Plaintiff’s Complaint states that “Plaintiff declares the full amount payable under the note and mortgage to be due.” Ms. Hunt did not know what that meant.

Mr. Rosen: Q. Okay. What does it mean in number 8 that the plaintiff declares the fill amount payable on the note and mortgage to be due?

. . .

Lona Hunt: A. I’m not sure.

(Hunt Depo, P. 51 Ln. 7-13).

Paragraph 9 of Plaintiff’s Complaint states in part that “[s]aid indebtedness has been accelerated pursuant to the terms of the subject note and mortgage.” Ms. Hunt also did not know what that meant.

Mr. Rosen: Q. What does indebtedness has been accelerated, what does that mean? It’s in paragraph 9, second sentence there.

. .

Lona Hunt: A. I’m not sure.

(Hunt Depo, P. 51 Ln. 18-22).

She later admits twice that she did not know whether a notice of default/acceleration letter had been sent.

(Hunt Depo, P. 58 Ln. 22 – P.59 Ln.12).

Paragraph 10 of Plaintiff’s Complaint alleges that Plaintiff is obligated to pay its attorneys a reasonable fee for their services and that Plaintiff is entitled to recover attorney’s fees to statute and the promissory note. Again, Ms. Hunt did not know that to be true.

Mr. Rosen: Q. How did you know the plaintiff is obligated to pay its attorneys a reasonable fee for their services?

Lona Hunt: A. I don’t know. Can you repeat what you mean?

Mr. Rosen: Q. Sure. I’m just asking paragraph 10, how do you know that plaintiff is obligated to pay its attorneys a reasonable fee for their services?

Lona Hunt: A. I don’t know.

Mr. Rosen: Q. And how do you know the plaintiff is entitled to recover its attorneys’ fees pursuant to Florida statute and the promissory note?

Lona Hunt: A. I’m not sure.

(Hunt Depo, P. 51 Ln. 24 – P. 52 Ln. 10).

Additionally, Ms. Hunt did not understand the term “deficiency judgment” found in Plaintiff’s pray for relief, the wherefore clause.

Mr. Rosen: Q. What is a deficiency judgment? In the wherefore clause it says deficiency judgment. What is that?

. . .

Lona Hunt: A. Not sure.

Some may argue that the terms which Ms. Hunt was unfamiliar with are “legal conclusions” and that she does not have to be familiar with those terms. However, this argument is preposterous! The document Ms. Hunt was verifying is a legal document, with legal terms to describe the factual allegations to which Ms. Hunt swore were true and correct. If Ms. Hunt does not understand the very basic terms of her employers business, she cannot possibly truthfully and accurately verify the allegations of the complaint and must not sign, under penalty of perjury, otherwise.

As a very astute judge once said to me, until someone goes to jail, nothing will change. It’s infuriating that banks continue to break the law. However, in this instance, no words can describe how outrageous this conduct is. Here Fannie Mae and Seterus, through their robo verifier, are breaking the very law with the same conduct that necessitated this particular law in the first place. It’s like a ponzi schemer, raising money to pay investors by ripping off new ones, or a drug dealer posting bond by raising money selling more drugs. Quite simply, if swearing under penalty of perjury, that you read something while later freely admitting, twice, that you did not, is not a crime, I don’t know anymore what is. If I did this, I’d expect to be charged with a crime but for the banks, I suspect this will just be treated as another “mistake” or “paperwork irregularity.” It is neither of those things. THIS IS A CRIME AND IT SHOULD BE PROSECUTED LIKE ONE, FROM THE HIGHEST LEVELS OF FANNIE MAE AND SETERUS, WHO ARE PUTTING ROBO-SIGNERS IN A POSITION TO COMMIT THEM. Here it is Pam Bondi and others, crystal clear proof that a crime has been committed. QUESTION IS – ARE YOU GOING TO DO ANYTHING ABOUT IT?

~

If you are in Florida and are looking for help with debt and foreclosure, call us at (855) 55-ROSEN or fill out our online form for a FREE CONSULTATION. Let the lawyers and staff at The Law Offices of Evan M. Rosen serve you!

~

Full Deposition of Lona Hunt