- Contact Us Now: 754-400-5150 Tap Here to Call Us

Foreclosure Fight Club: Another Trial, Another Win by The Law Offices of Evan M. Rosen (Part 1)

Foreclosure Fight Club: Another Trial, Another Win by the Law Offices of Evan M. Rosen (Part 1)

It all started a little over a year ago when a husband and wife contacted our firm about a foreclosure. They were, and still are, facing the same struggles as millions of other Americans in the aftermath of Wall Street’s financial game that ended with the bailout for them and busted home values and foreclosures for millions of citizens. Their mortgage loan was taken out in 2008. Just like almost everyone else who took out a Wall Street housing bubble era mortgage, their loan was deeply underwater. After running out of options and getting the maddeningly familiar loan mod run around by their servicer they could no longer keep up with their payments. They came to us for help with the fear and dread of an impending foreclosure judgment looming in the near future. They were victims of sewer service, a practice in which parties to a lawsuit are never served but the case is moved forward based on an affidavit of a process server claiming the house was abandoned and the defendants cannot be found. Upon learning about the lawsuit they acted immediately to get the situation rectified by hiring the Law Offices of Evan M. Rosen.

Shortly after filing our motion to quash service, we got the defaults vacated. Then the case moved fast. After all, it’s a Miami-Dade case. Our preliminary motion to dismiss was denied. Then, we filed an answer and affirmative defenses. Shortly after that, what do you know, we received an Order from the Court Setting the Non-Jury Trial.

So with the case being set for trial, our staff went into in-depth research mode. I am confident that we have some of the best researchers in the business.

One of the first areas our team dug into was the fact that this particular loan was a FHA loan. This fact, little did we know, would take us down a path of “HUD asset” sales in which the federal government was trying to reduce losses from mounting foreclosures.

U.S. banks — especially smaller regional banks — have a lot of non-performing loans on their books. Loans are considered non-performing once 90+ days past due. But the U.S. government — one of the biggest players in the residential real estate market — has a lot of non-performing loans too.

The U.S. Department of Housing and Urban Development (HUD) will sell $1.7 billion portfolio of non-performing Federal Housing Administration (FHA) loans in September as one of the largest deals of its kind, ushering in the most significant pickup in supply of the distressed debt since the beginning of the 2008 financial crisis, according to DebtX, the loan sale adviser retained by the federal government to orchestrate the sale. The federal government is trying to reduce losses from mounting foreclosures.

On Sept. 12, sealed bids will be accepted on 13 pools of non-performing loans in some of the hardest-hit housing markets, including Chicago, Newark, N.J., Phoenix and Tampa. Buyers expected to bid on the distressed debt include Santa Ana, Calif.-based Carrington Capital Management, Fortress Investment Group (FIG), PennyMac Mortgage Investment Trust (PMT) and Selene Finance, a firm controlled by former Salomon Brothers bond pioneer Lewis Ranieri.

HUD created its Distressed Asset Stabilization Program in 2010 to safeguard the FHA’s insurance fund while helping seriously delinquent borrowers avoid foreclosure. Under the program, non-performing FHA loans are sold for less than the borrower owes, which gives investors the flexibility to reduce the principal or modify the loan’s terms. Investors who buy the distressed debt have to wait six months before proceeding with a foreclosure.

Another article we came across showed that these loans were being purchased at steep discounts.

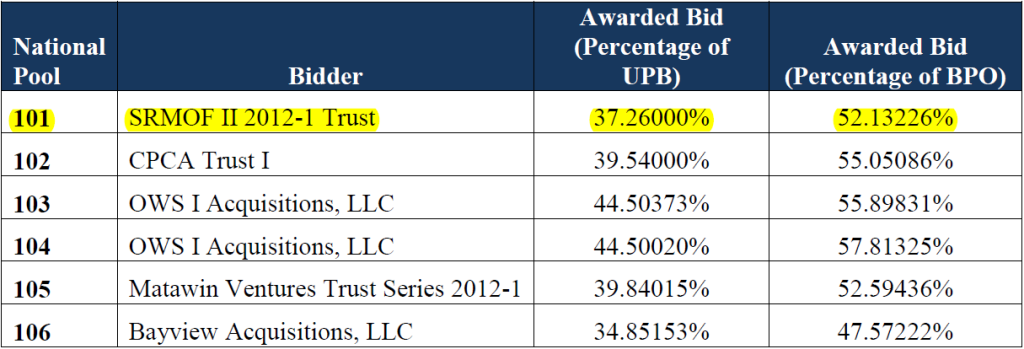

HUD’s September sale took place in two parts. The first part, conducted on Sept. 12th, consisted of 5,300 non-performing loans in six different “national” pools with a combined unpaid principal balance of $950 million. Winning bids went from 34.9 cents on the dollar of the unpaid principal balance to 44.5 cents.

Affiliates of Minneapolis-based Castle Peak Capital Advisors won the largest pool of 1,392 loans with an unpaid principal balance of $239.4 million with a bid of 39.54 cents on the dollar. The second part occurred on Sept. 27th and consisted of 4,100 loans in seven different “Neighborhood Stabilization Outcome (NSO)” pools with a total of $770 million in unpaid principal balance. Winning bidders paid on average 32 cents on the dollar

Blackstone affiliated Bayview Acquisitions LLC was among the winners in that group paying 26 cents on dollar of 1,430 loans with an unpaid principal balance of $269.1 million.

With this information now in hand, our staff went to work on trying to find out if our client’s loan was a part of the above named pools.

We knew who the plaintiff was from the complaint, a servicer, but who was the owner of the loan? Who was the real party in interest?

A quick search on the MERS MIN look up tool revealed it was a Ginnie Mae Trust which lead us to HUD’s Single Family Loan Sale Initiative.

SFLS Objective: The SFLS Initiative intends to meet the mission and financial objectives of keeping homeowners in their homes, reducing claims costs, minimizing the time that assets are held and maximizing recoveries to the government on the sale of these assets.

But was our client’s loan in one of the above pools?

To find out, we called our contact who works for HUD’s Asset Management Division and gave her our client’s FHA Note# and were told the note was sold in the September SFLS initiative bid to Castle-Peak with effective sale date of November 29, 2012.

Further research confirmed Castle-Peak purchased the Ginnie – FHA pool with our client’s loan at a a substantial discount and FHA paid the insurance claim to Flagstar on November 29, 2012. Then, without any advance warning, a representative from FHA, connected us directly to the owner of the loan! Unfortunately, the Florida Bar rules prohibit an attorney from speaking to someone who is represented by counsel about the subject matter of the case. Our research, as well as correspondence from the new servicer revealed that the new owner had a new servicer, which was different from the current plaintiff. Still, our staff immediately asked if this person was represented. The owner initially said no and told our office that they were willing “to make a deal which included a principal reduction”. Although we were thrilled he was so eager to negotiate, our staff asked again if the owner was represented. This time he said he wasn’t sure. He then repeated that he wanted to discuss and resolve the matter but out of an abundance of caution, our office had no choice but to end the conversation, without discussing anything further other than my ethical obligation not to speak with him about the subject matter of this case as he might be represented by counsel.

An exception to this bar on communications is if the attorney grants their consent. So, we asked opposing counsel for consent to speak to their client but they could never verify the identity of their client! As is typical (and insane), plaintiff’s lawyers only know and deal with the “servicer” not the real party in interest. It’d be like me filing bankruptcy for Ms. Jones while only talking to and gathering info from her son. The telephone game proves some messages will get botched and most lawyers have a strict policy to only communicate with that client and no one else, for more than one reason. Another example of how things are “different” in foreclosure world.

So we continued with our background research. After looking at reports from HUD, we discovered that our client’s loan was in the pool that was purchased at an aggregate 37.26% of unpaid principal balance.

On this particular loan, our client had an outstanding principle balance of $212,000.00 with the home being assessed at $96.000.00 by the Miami-Dade Property Appraiser.

Knowing that the new investor paid an aggregate amount of 37.26% of unpaid principal balance, or about $79,000.00 for this loan, and this program was designed to allow “investors the flexibility to reduce the principal” and “keep homeowners in their homes” we set out to try to resolve the case with opposing counsel before the trial date, which was about a month away.

We thought this would be easily resolved since the new owner of the loan was so eager but it was not. No reasonable modification was offered from opposing counsel, who probably had no idea about the above, and a deal could not be reached.

A loan mod was offered but it was vague and lacked specific loan details. There was no mention of what the new principal balance would be or if it was increased or decreased, no specified interest rate, no terms regarding property insurance and taxes, no mention of escrow, nothing on the new maturity date, and nothing about the total amount of a balloon, forbearance, or deferred principal. No details or specifics whatsoever. Just an “offer” for our clients to pay $1,760 a month for six months and then they “might” consider reviewing a modification application with a forbearance of fees and interest leaving them with an amount due of hundreds of thousands of dollars more that the property was worth. Oh, and one other detail. Should we accept this “illusory” deal, we would also have to agree to forever waive our defenses. We reviewed with our clients and rejected immediately.

Then another offer was made – $4k cash for keys, waiver of Deficiency and a 90 day sale date. Both of our clients are gainfully employed and want to pay to keep their very modest home.

Since neither offer helped our client achieve their goals, once again, we contacted opposing counsel, to see if they would be willing to give their consent for us to speak with the loan owner, Loan Resolution Department, and/or servicer, directly for purposes of working out a loan modification.

Again, they did not know who the real party in interest was but whoever that was, they would not give their consent. As is often the case, we knew at that point that we knew far more about this loan then the plaintiff’s lawyers!

Not being bound by the Florida Bar, our clients then called the servicer and owner of the loan themselves. However, upon contacting the owner’s rep, they were told they needed to “ditch their lawyers and then they can get a deal, but with lawyer they get nothing.” So they said fine we ‘ll ditch our lawyer and then the owner stopped returning calls.

With communications at a standstill and only some meaningless, unenforceable, “illusory” loan mod offer on the table, our clients wanted to have their day in court and we were glad to honor that request!

Earlier in the case, we knew, initially from letters sent to us by Selene, that the servicer of the loan changed from Flagstar to Selene. Flagstar was the plaintiff in the case. The plaintiff moved to substitute Selene for Flagstar but it was denied for failure to appear to their own hearing. The Plaintiff also failed to comply with Court’s Orders, failed to serve two Trial Orders, and filed three false Certificates of Service.

On December 12, 2012, the Plaintiff filed their Trial Witness and Exhibit List. It stated, inter alia (a fancy way of saying among other things), that a “[r]epresentative of Plaintiff will testify as to the business records of the Plaintiff…” It listed no names and no addresses, in violation of paragraph 3(a) of the trial order. On March 25, 2013, Defendants filed a Notice of Request to Make All Trial Exhibits Available and sent two follow up e-mails on March 25 and March 29, 2013, asking for copies of exhibits. (See attached Composite Exhibit A.) In violation of the Trial Order, Plaintiff failed to make its exhibits available. Further, the Defendant’s counsel was notified, only moments before the April 12, 2013, trial that the witness the Plaintiff intended to call was not a “representative of the Plaintiff” as was disclosed in its List.

The failure to follow the Court’s orders as it pertains to not making exhibits available, not disclosing the names and address of its witness, and the prejudice caused to the Defendant by these violations were raised at that start of trial on April 12, 2013, via an ore tenus Motion to Strike the Plaintiff’s Witness List. The Court denied that motion but continued the case until August 23, 2013, giving the Plaintiff another chance to comply.

On June 19, 2013, and again on July 29, 2013, the Plaintiff filed a Trial Witness and Exhibit List. It again stated a “[r]epresentative of Plaintiff will testify as to the business records of the Plaintiff…” The one dated June 19, 2013, listed no names and no addresses, again, in violation of paragraph 3(a) of the trial order. The July 29, 2013 list gave five names but, in violation of paragraph 3(a) of the trial order, gave no addresses. Again, moments before the August 23, 2013 trial, the Plaintiff first notified the Defendant that the witness was not a representative of Flagstar but was instead an employee of Selene.

From the August 23, 2013 Trial Transcript:

MR. ROSEN: Your Honor, there are five things before the Court’s consideration that all pertain to a Motion to Dismiss or a Motion to Strike the Witness List. This is the third time we’re here. There were two prior trial orders.

Since that time, there has been three witness lists. All of which name the Plaintiff’s representative. The Plaintiff is Flagstar Bank. In June, there was a Motion to Substitute filed by opposing counsel, set for hearing. They didn’t show. You denied their motion. I was there.

Since that time, another witness list has been propounded again listing the Plaintiff’s representative. I find out again this morning it is not from the Plaintiff. It’s from a different entity altogether.

The loan has since been sold and transferred. The new owner of that loan has a new servicer who is here today. The true Plaintiff in this case is not present, nor is their representative present. At the prior trial, we brought this up and Your Honor was kind enough not to strike their witness list, instead give a continuance to where we are today. I’m bringing up the exact same issue all over again.

Furthermore, Your Honor, there were two trial orders which we were never served with. I spoke to opposing counsel about that this morning. One of which, apparently, she didn’t get either.

Lastly, we had filed a Motion for Sanctions, which was resolved at a prior point by agreement because there were three certificates of service, actually four, alleging that they served us the trial order and we never got them. They were false certificates of service.

I reached out to opposing counsel three times. After the third one is when I finally said okay, enough is enough. I’ve tried. I’m going to file a Motion for Sanctions. You guys are lying to me and the Court about what you’re serving.

After hearing this, the court was furious and decided to special set the trial for the next week.

THE COURT: 7:30 Tuesday, we can bring all the motions. I’m going to tell you right now. I do not issue orders for people to disobey them and I have been known to sanction people a lot of money because I believe that the only way that I can get people to comply is to make it hurt.

OPPOSING COUNSEL: Yes, Judge. I understand.

THE COURT: So whoever shows up, beware that if I find that my orders have not been complied with, there’s going to be hell to pay.

We filed our motion for voluntary dismissal and with great anticipation started preparing for the upcoming hearing.

To be continued…

Foreclosure Fight Club: Another Trial, Another Win by The Law Offices of Evan M. Rosen (Part 2)

If you are in South Florida and are looking for help with debt, foreclosure, student loans, real estate or want more information about bankruptcy law, call us at (754) 400-5150 or fill out our online form for a FREE CONSULTATION. Let the lawyers and staff at the Law Offices of Evan M. Rosen serve you!

If you are an attorney looking to improve your comfort level and trial skills in order to better serve and represent clients in defense of foreclosure, our workshop will help you. If you have any questions, feel free to contact us at 754-400-5150 or erosen@evanmrosen.com.

Foreclosure Trial Workshop October 19th – 20th Registration

Redacted Motion for Involuntary Dismissal With Exhibits